There are two personal characteristics that make a material difference to who you are going to be in life. These aren’t hard skills, but core traits of humanity.

hustle and curiosity

Both are now essential in 2026.

We live in by far the most unpredictable, volatile, fast-moving moment since the Berlin Wall, and it’s completely unclear where we are heading. Anyone under 40 years old has no direct experience of anything like this and they should listen today.

Curiosity comes from all the daily inputs around us. An overheard conversation on a train, a mate’s DM, the scroll of a well-curated timeline, a casual comment from your kids (like Clavicular last month).

The good news is that there are a lot of those inputs now, and they usually have a pattern, or some kind of message. The skill is in seeing the connections, filtering out the noise, and perceiving where the news cycle is leading, before you get run over.

The people who can do that are called visionaries and this is their time.

The relentless gravity of Mountain View.

This is what buzzes around my head as I sit here, overlooking a lake:

Google search traffic to publishers is down a third in the last year. Has it actually killed journalism as a business, and is that a glance into sports future?

Why didn’t YouTube get those extra NFL games? Have they got any coordinated plan about sports? Or do they just know exactly what is too expensive? How is that new guy from Disney getting on?

Jeez, it’s a risky business investing in innovation these days. Google can ship some new product overnight and you are fucking toast.

AI is about to change absolutely everything, and this is bigger than the Industrial Revolution. Even the Pope has now put out an Enciclica, and those are very rare. This is the big moment, full of both opportunity and risk. Good and evil.

My company has put me on an unlimited plan for AI use. I’m no longer restricted by tokens. My power is now limitless!

The hardest thing to do in business is manage Innovators’ Dilemma, especially when you are sitting on the greatest business model the world has ever known. So, how do you as a listed company push Gemini, when all your revenues and marginality comes from Search?

Everyone talks about Elon, but Waymo is still flying under the radar. Why?

These 3 upcoming IPOs are totally detached from any idea of traditional corporate finance or capital markets. It is Alice in Wonderland capitalism. Where do you put your money? What do you think of Alphabet? Are you an investor at this valuation?

Yes, today’s Albachiara Column needs to be about Alphabet/Google/Youtube(YT).

Because this company, almost uniquely, touches every facet and major trend of our business lives and leisure time. And that’s now going to increase. If one of the principal Albachiara axioms is to know everything about the people who materially affect your business, serious sport execs need to think very hard about the Kingdom of Page and Brin. At 360 degrees.

This is not about the “micro” of AI product functionality, the power of YouTube, or even the future of AdWords and the open web; it is about the “macro” vision of where this whole group is going, and why. And where it will leave sport, the markets, the world of work, and humanity itself.

It is all insanely complex and interconnected, even within Google. Frankly, they too are feeling their way, with workflows and processes now bouncing off the walls. The entire organisation is in “high hustle” because the stakes are just so huge and time is short.

Let’s today try and unpack it all, and then hopefully reassemble a conclusion. Just don’t expect a tightly edited piece. We are all struggling to order wtf is really going on, and this will be no different.

So we are going to jam a bit, and go with the flow.

Google/YT and Sport.

We shall start close to home.

In AI time, 18 months is an eternity, and our previous piece Don’t be evil, from October 2024, now seems like ancient history. Many, at the time, were highly dismissive; but since then, all roads have indeed led to YT. And then some. There isn’t a sport or broadcaster on the planet who hasn’t had to rethink where they now stand in relation to the Google video platform. It’s where the mass market eyeballs are, and everyone has now finally got that memo.

We are bombarded with thought pieces and podcasts.

**

Broadcasters and sport bodies unable to move without first working out their YT strategy and tactics.

***

Rights holders using the platform to address audiences better than the old distribution model of overseas monetisation.

Bibliography:

* CazéTV will broadcast LaLiga in Brazil for the next six seasons

* Why does Mark Goldbridge have Bundesliga rights?

****

The intertwined complexity around carriage deals with YouTubeTV and the sports channels.

Fat and skinny bundles.

*****

The debate from 18 months ago, around the inevitable centrality of YT, has been won, and it wasn’t even close. But the world has moved on, a lot, and a new question is now way more pertinent for our industry.

Aside from the eyeballs KPI, can anyone make a sustained sports business in a world where YT is your main distribution platform, the gatekeeper, and they don’t pay the rights fee you have always expected? Leaving aside all the marketing, funnel, attention, engagement blurb… where’s the serious beef?

Where’s the YT beef?

This is a follow-the-money CFO objection and the thrust of Peter Hutton on this month’s Citizen AYNE. It now needs answered if we are to be professional as an industry. There are some very obvious questions to ponder:

*

Is the strategy of Google and sport in the USA as different to Europe as it seems to be? If the answer is yes, and it is, what does this tell us about the trope of our sector as an asset class? The US can make sport work so much better because of a more advanced advertising market, higher CPMs, organised sales forces, and a bigger TAM. This is why Big Sport is still on terrestrial TV there. Mark Oliver explained this so well on the first Citizen AYNE. Are YT ad inventories outside America seen as premium? If not, can they be? How much actual juice is in ads as a revenue model?

**

Is the YT membership scheme a credible substitute to a subscription model? An owned-and-operated DTC strategy? Why aren’t clubs using this much more? Even if it’s an option, who owns the data? Can we trust these techies?

***

Does YT have the resources and urgency to invest into the sales and account management teams needed to service sport on their platform? Or are you left on your lonesome with one of their “how to” videos as your only onboarding? Is there a mature enough ecosystem of agencies and collaborators?

****

Is YT just much more interested in how AI affects the creative process, and how they can leverage that?

Exaggerating to make the point, let’s always ask whether all the back-slapping press releases around YT are really just a signpost that the sport in question couldn’t get a normal rights deal away! Is doing something innovative and cool on YT therefore just a fig leaf for the poor sods out of other options? Is the Bundesliga still doing the Goldbridge deal if TNT Sports makes them a decent bid for UK rights?

YT in June 2026 does not pay upfront money for most sports, in anywhere close to what this industry needs to budget and pay for athletes. They would rather partner than acquire, and that is not going to change. Observe their deals with the World Cup. Look at how they like Caze TV.

YT outside the States is a friendly facilitator to achieve its own aims, and it is not going to war, or into rights auctions. They have tried, and can’t make the numbers work. They remain for us a cost-of-customer-acquisition marketing play to attract all those newer audiences, in the hope that one day they will convert as a subscriber. Or go to the live event. Or buy merch.

And maybe that’s fine.

Friend or foe?

To quote Sir Martin Sorrell 20 years ago, a bit of both,

Google are frenemies; an ad agency, media owner, and platform, all rolled into one.

In this moment, now also with Google Cloud services and AI, things are even more unclear, and we are only in the very early innings of finding out. But one thing is surely true. Google cannot be ignored by sports, and should be seen as a true partner for mutual benefit.

That needs very clear pragmatic case-by-case thinking on objectives, because our industry would have to change its entire risk-adverse B2B mentality. And it can’t do that with players to buy. Our industry only works today with certain upfront monies from a media rights fee, and Mountain View just isn’t in that game.

In short, we mustn’t lose sight of what is really additive to us with Google, and what is just fluff. We need a cold position on what is cannibalisation, because we have been here before. Exactly here.

And it is gross negligence to not learn from history.

The carcasses of the music and publishing industries.

I have had the privilege of a front-row seat in these two major IP industries eviscerated by the Internet. Once at EMI as an incumbent, and once at GiveMeSport as a disruptor. I have seen rivers of blood, and am therefore credible as a witness.

I even saw what was counted and accepted as a bonafide video view for sale. Sheesh!

In the week when once new-media darling, Buzzfeed, was sold for a song, we are all forced to accept that the whole idea of digital publishing as a business has failed. Certainly as an ad business. (Some people may point to the subscription model of the NYT or FT, but those are often expense account corporate buys not coming out of people’s personal disposable income. And so many are on starter subscription deals, that they will cancel when the full price is applied later.)

Let’s be honest.

The social platforms like frenemy Google sucked the entire soul out of the business model of writing and publishing. Even Runway in Devil Wears Prada 2 is now a shell. The promises back then of a win/win didn’t play out for the incumbents like Runway, or even the innovators like Buzzfeed, VICE, Vox Media, GivemeSport. These companies were all tempted by the apparent ability to reach infinite new audiences and readers online.

Forget possible cannibalisation, you need those customers of tomorrow. Your old readers are dying. The revenues will eventually come.

Sound familiar?

But everyone missed two existential points.

1.

The platform upon which you publish isn’t yours, and they can change the algo overnight. Your reach then craters.

2.

The ad inventory story was always “fugazi”. Digital publishing is an industry built on a $150b fraud misunderstanding that no one wanted to contest; certainly not the lazy media buying agencies who had client budget to deploy into those video views. Sorry, but you all know this to be true. You just have had no incentive to call the emperor naked.

And Google in all this?

The title of our first YT Column was Don’t Be Evil, being the original corporate motto of Larry and Sergey. Obviously that slogan needed to be phased out and it was, in 2018.

Because in business, at the very highest level, you have to have the coldness to commit murder when required. Or at least run your studs down the other guy’s shin. You need to be a killer.

Google has indeed killed, and one cannot make the case for the prosecution better than this wonderful piece from serial web entrepreneur Paul MacDonald. He is one of the brightest children of the Buzzfeed generation.

No matter how much one can like and admire the people at Google, they have blood on their hands. If not murder certainly passive manslaughter. But they also can have no blame because that’s the Logan Roy reality, and this is the life we have chosen. The animal spirits of free markets. Bayonet the wounded.

In these years publishers cannabilised their analogue product by putting everything on the web in search of new audiences, in the belief of digital ad revenues. Substitute “publishers” for “sport”, and that is what we mean by the new question sport needs to ask about YT. Because the parallel with publishing and music is too close for comfort.

Never forget that kids have grown up with the idea that all content is free, and they will never pay a sub. They can’t even understand the concept. A quick look at the piracy stats on the Champions League final in the UK tells you all you need to know. These wonderful new audiences also have next-to-no patience with ads, and will grope for that “skip” button with impunity. Sadly it’s now getting much worse with AI. Web scrapers are gorging themselves on publisher content to put into Large Language Models (LLMs), and this represents yet another grand theft of intellectual property. Money the content creators will never see.

The arrival of AI changes everything in the creative industries including sport, and Paul this very month writes a truly devastating piece about the future of the web. Best not look if of faint heart. The magnificent Julie Alexander opines in a very similar vein here, as the greatest business model in the world, “search”, is now evolving at pace.

And that right there is the Google priority. Not sport.

This is going to be a tough business for us now.

What about Sport-Adjacent and Google?

Google affects our industry every way we turn.

Somewhere, in the “asset class” known as sport, is an investment theme known as sportech. Various types of software companies and products called “enablers”. These aren’t an IP play, but it’s still sport investing, with evermore funds looking for such opportunities. The established wisdom these days is to invest to combine IP ownership with enabling technologies.

Meanwhile, Alphabet/Google is on a mission to ship shiny new product at light speed, all coming out of the talent they have in-house, especially in AI. They have serious human resource in there, and for a true understanding of the endless reach and power of Google, and how we got here, this Acquired podcast is so so good.

Podcast description

Google invented the Transformer – the breakthrough technology powering every modern AI system from ChatGPT to Claude (and, of course, Gemini). They employed nearly all the top AI talent: Ilya Sutskever, Geoff Hinton, Demis Hassabis, Dario Amodei – more or less everyone who leads modern AI worked at Google circa 2014. They built the best dedicated AI infrastructure (TPUs!) and deployed AI at massive scale years before anyone else. And yet… the launch of ChatGPT in November 2022 caught them completely flat-footed. How on earth did the greatest business in history wind up playing catch-up to a nonprofit-turned-startup? Today we tell the complete story of Google’s 20+ year AI journey: from their first tiny language model in 2001 through the creation of Google Brain, the birth of the transformer, the talent exodus to OpenAI (sparked by Elon Musk’s fury over Google’s DeepMind acquisition), and their current all-hands-on-deck response with Gemini. And oh yeah – a little business called Waymo that went from crazy moonshot idea to doing more rides than Lyft in San Francisco, potentially building another Google-sized business within Google. This is the story of how the world’s greatest business faces its greatest test: can they disrupt themselves without losing their $140B annual profit-generating machine in Search?

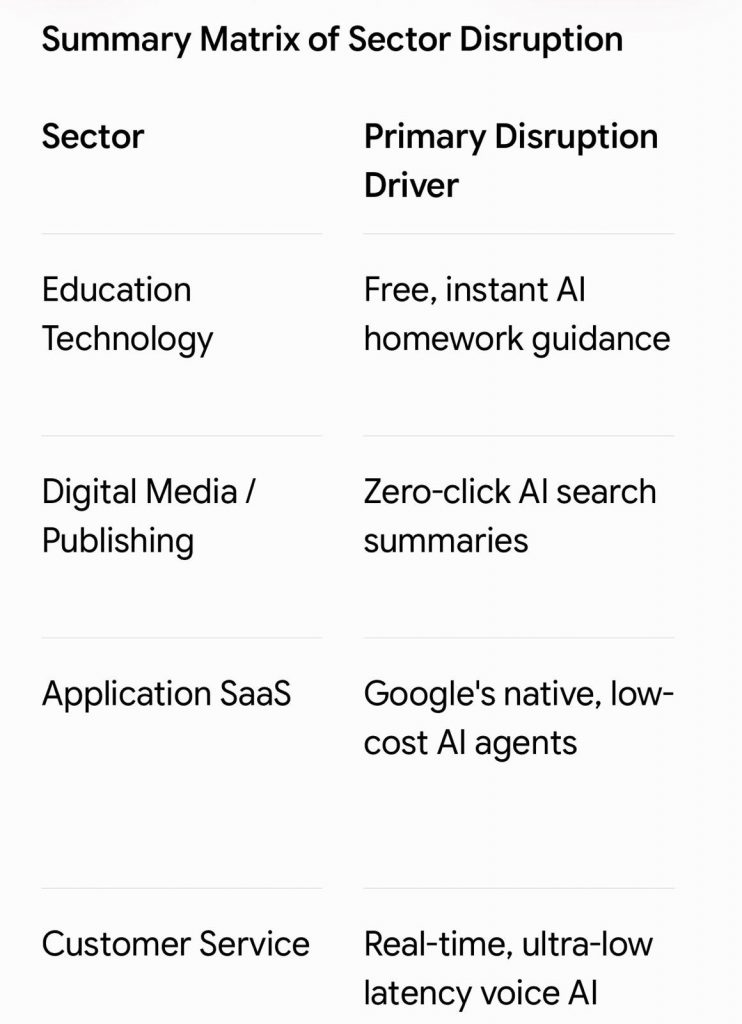

The pace of this innovation and disruptive change is mind blowing, and any one of these new Google products could be fatal for the sportech start-up you just invested in.

Lights out.

There is therefore no debate that the risk profile of such investing is way higher than 18 months ago, with so many data-points to confirm this thesis. Familiarise yourself with some of them, to see loads of risk capital burnt overnight.

Figma suffering from Google Stitch.

The effect of the introduction of Genie 3

The examples everywhere are dramatic.

And in sport? Try this one. Look at the 3 questions posed in this infographic.

Of course Google hasn’t prioritised this product as yet. It could, but likely doesn’t need the aggro or distraction. They prefer to prioritise partner relationships for now, rather than unleashing hell!

But there is no doubt whatsoever that the entire outlook for innovation in sport, VC-funded, has no relationship to the set-up we had 5 years ago. It is much harder, and much riskier, at exactly the same time the number of funds chasing such deals has increased.

That’s the perfect recipe for malinvestment.

So what actually is Alphabet/Google/YT today?

Google is not a media IP company, far less sports jocks, and there is a famous running joke in their offices.

“If you’re not an engineer, you are getting a free lunch.”

Google has built its dominance and fortune as mainly a tech platform to serve ads on the back of search queries. It now also has a growing Cloud business similar to Amazon AWS and Microsoft Azure and is integrating AI into all of this, hopefully without undermining those amazing cashcow revenues. That’s their Innovators’ Dilemma and, even per se, a fascinating case study.

So sport is a pimple on its arse, way way down their list of priorities. It’s a piece of content that either works, to generate ad revenue, or it doesn’t. At best maybe a simple channel of extreme fan loyalty to sell the Cloud and AI products into. All this shows in how they have approached buying sports rights. They only bid when the numbers work, and/or if really scared of Amazon or Netflix. In Europe they don’t bid at all. Peter Hutton saw this same reality all too clearly at Facebook.

These platforms are not in love with sport. We need them more than they need us, and we will have to play very smart to not just be collateral damage in this new AI war, with all its enormous capital needs.

As yes. Artificial Intelligence.

AI AI oh!

This arrival of AI is not a normal technological advancement. It is a true pivotal crossroads in the history of civilisation and humanity, and even the Vatican perceives this. The Catholic Church has lasted 2000 years because it always knows how to recognise the big moments of change.

But separating the true realities of AI from the hype is difficult. We all see what the products can do, we all lament the layoff of colleagues now considered superfluous, we fearfully listen to those on the front line who tell us coldly that we can’t conceive the change about to hit us all.

Marc Andreessen is one of the most accomplished tech founders and investors around, and it is simply impossible to brush off what he is saying. For what it is worth, I tend to agree with him.

But he is not alone here. The previous Google CEO is so worried about all of this that he advises us to pull the plug whilst there is still time.

These are big statements, and here is the current Google CEO with another little ditty.

They are admitting they don’t know what is happening.

And you don’t think that’s scary?

As a technological leap, this is like the arrival of the wheel, the steam engine, or the printing press. Huge gains in human productivity, except this time maybe the human is no longer needed as part of that equation?

Elsewhere, however, the elite finance community warns about how all this capital investment (capex) in AI infrastructure will never ever make a positive return on investment. My own podcast buddy Grant Williams looked into all of this a full year ago, and he is always the most insightful voice out there. (He generously puts this amazing piece in front of his paywall for us today. Don’t miss it.)

These sceptics will correctly say that the tangible financial impact from AI at companies is still woefully marginal, both on the revenue growth side, and even the cost efficiency side. And that all these hundreds of billions of capex dollars into datacentres will never offer a substantive payback and return. The unimaginable fortunes lost will be soon seen as the biggest bonfire of the vanities ever, and when that hits, it will drag down entire economies and stock markets with it.

All this is the most significant macroeconomic event of our lifetime, and also the central plank of the geopolitical death match between the USA and China, as Prof. Galloway notes. China could go to war by “dumping” cheap AI into the markets of the West, and then watch the whole capitalist Jenga Tower collapse.

What a time to be alive!

Yes, you can see evidence everywhere that the AI business model doesn’t work, or pass the test of the serious corporate financier, and that’s important. Especially true for the specialist players like OpenAI, Anthropic or Perplexity who just don’t have free cashflow from other business lines to pay for the investment.

These guys are flying on fumes, and yet these are exactly the ones coming to the capital markets with enormous IPOs later this year, all with simply preposterous valuations. They, together with our old charlatan buddy Musk, and his SpaceX, are asking us all to go down the rabbit hole and fully suspend our intelligence.

The smart commentators see all of this, but the sheep will cheer these three IPOs with gusto. Just as they often do with all these absurdly overvalued media rights deals and franchise valuations.

Is Alphabet going to get dragged down?

Let’s put the accountant’s hat on.

Unlike some of its AI competitors, Alphabet is a very solid listed company, with a healthy balance sheet, valued at around $4.5 trillion, representing a multiple of 11x revenues, and 29x profits. That’s a chunky valuation by old standards but it is in line with similar companies, and arguably comparitively cheap, reflecting its near monopoly and full moat on search.

Consolidated revenues are over $100bn a quarter, with high growth.

*

70% of that revenue is advertising related, including YT, mostly from “search”. This part is still growing at a very healthy 21% and that is so important to digest. Search revenues as yet are not under pressure from AI, as many feared. With the integration of Gemini 3 Flash and Nano Banana, it has so far more than maintained its search dominance.

**

Google Cloud, a direct competitor of AWS and Azure, accounts for nearly another 20% of revenue. This division is in hyper growth, (63%), driven directly by enterprise AI solutions and token consumption. Deep analysis shows that Google is winning the AI wars, and this is the kernel of today’s research. Google is getting stronger.

***

Google subscriptions and Platforms add little.

****

Other bets like Waymo contribute nothing material for the accountants as yet. But finance is not accountancy, so put a flag here. This is upside.

Consolidated profits are $40bn a quarter, and that is a blended gross margin (40%) to die for.

So Alphabet is not a meme stock and is the best placed of all to endure the bloody attrition of AI investment.

And attrition it has to be, especially to defend their “search” golden goose. They are just utterly obliged to commit enormous amounts of capital expenditure (almost $200bn a year) to build out data centers and TPU (chips) infrastructure, to compete with rivals doing exactly the same thing.

But Google will win this war.

The widening moat around the Kingdom.

It’s about the barriers to entry, stupid, paraphrasing Bill Clinton. Aka moats.

Growth without a moat is like the airline industry: volume expansion for 100 years and basically zero cumulative profit.

PS: Substitute “European football” for “airline industry” and this statement hits hard. We in soccer have grown enormously as an industry over the last 30 years but have made nothing but losses. Because there is no moat with open sports leagues. Promotion and relegation is the bridge over the moat and that is devastating for any “asset class”. No-one seems to care.

Google with AI instead has now significantly increased its moat on search. It is a fully integrated supply chain which none of its competitors has. It is unique, with also the outrageous privilege of having the platform of the world’s eyeballs as a funnel. That’s called YouTube.

A genuine shiver goes through my spine as I write this. The hairs on the arms. This is all fucking genius and the killer riff.

I check I’m not getting ahead of myself and I find this amazing video that summarizes everything. This is the standard of analysis out there now and AI is indeed a limitless superpower for a hustling and curious brain. Please do yourself a huge favour and give it 16m. You will never need to listen to any other podcast on AI.

Our slightly creepy German friend here does a truly wonderful job noting that this isn’t about the product announcements. It’s just much bigger than that.

He concludes that Google is a great business but it is fully priced already. Priced for perfection. He however does not mention Waymo, which is an error.

The “Other Bet” of Alphabet.

Read the full article here.

Elon Musk will make big news with his fraudulent IPO this year. Tesla is an absolutely busted flush as a business, whilst Mountain View is sitting on this jewel that no one factors into the Alphabet valuation.

So would I invest in Alphabet today?

This was one of the specific inputs at the top of the show today. And it is the acid test for any real commentator in business. Forget all your smart analysis. Would you risk your own money, buddy?

It is here I am legally obliged to repeat that this Column is not investment advice. It is for educational and entertainment purposes only. You should do your own research and speak to a professional adviser.

I have always talked about the crazily high valuations on all assets these days. The Everything Bubble is one of the key tenets of The Storm, and it has gotten much worse since we published the book. So no, I baulk at buying any company at 30 times profits, and would ideally wait for the macro to crash. But if I have to deploy capital into equities now then Alphabet is absolutely where I’d put it. No question. Seems Warren Buffet’s company thinks the same.

I am no longer worried that Google will suffer the fate of Kodak with Innovators’ Dilemma and lose its core search business. From whatever way I look, Google wins the AI war. Here actually is Google’s AI rival Claude confirming that 🤭.

Conclusions.

Ok. Jam session over. What did we get on tape?

*

Absolutely what a time to be alive. Hustle and be curious.

**

In another 18 months we will all have seen clearly the true power of what AI is going to do to our business and personal lives. SkyNet may even have used that “black box” to take us all to our maker. The Pope will smile.

***

Google is going to fulfil everything it promised when starting the Transformers journey, the DeepMind acquisition. They will utterly dominate the AI space as the others just can’t make the numbers work without the fully vertical ecosystem and moat that Google has.

****

Google Cloud will continue to grow like weeds in the garden. Token use in companies will explode. They will also manage to protect the cashcow search business and be one of the very first companies to ever solve the Innovators’ Dilemma.

*****

YouTube will continue to become the new TV and the centre of everything. It is the gateway to humanity. And the ideal channel for AI penetration.

******

Google and sport will toodle along. The USA will continue to be treated far different to the ROW. They won’t pay big rights for anything apart from the very top premium sport. And even then they won’t overbid. Every other rights holder will have to work out YT, mainly on their own, because Google ain’t dedicating resource to spoon feed them. YT will never replace the rights fee for most of sport and many will suffer the fate of the old publishing industry. Below the very top level, we will revert back to the pre 1990s, more around the live community experience. More local, more authentic and more sustainable. There is one upside. A silver lining. Google in AI is not a monopoly so it will need to spend serious money on marketing, and that will be obvious in the World Cup. They WILL also be open to technology partnerships with sports who embrace Gemini/Pixel fully (like Formula E). It’s a version of the new “quadruple play”. Gemini, Pixel, Cloud and YT.

*******

The capital markets in the next 6 months, with these 3 truly insane IPOs, with a new Federal Reserve Chairman, with the Straight still closed, are going to test us all. I absolutely fear the worst.

To order the Limited Edition of Roger Mitchell’s book “Sport’s Perfect Storm“, click here and fill the form.

Listen to our “Are you not entertained?” sport management podcast here.

To find out what we do in change management, have a look here.

For our C-suite management services, read here.

Here you can know more about our content development work.

Discover our Corporate Learning service here.

Get to know more our “Sport Summit Como” yearly sports management event here.

If you want to read our own story, go here.