The price of a barrel of oil is the most important variable in all of macroeconomics, finance, and geopolitics. That is not hyperbole.

For many people, and for various reasons, $80 is Goldilocks.

The Wisdom of Tommy Norris.

Landman is a recent, very successful Paramount TV series about the Texas oil business.

What it talks about, and the vocabulary it uses, is the best example we have of what many call the Trump Turn, especially in relation to energy policy. Specifically, the idea that there is no actual alternative source of power out there that can replace the black gold. Certainly not at any affordable price that works for business margins and competitiveness.

Narratives change. Be ready to adapt. Always.

It is not the strongest of the species that survives, nor the most intelligent. It is the one that is the most adaptable to change.

Charles Darwin.

After many unchallenged years of green and net-zero thinking, that change is now upon us. This dose of Landman Realpolitik was sorely needed, because truths may be unpalatable, but ultimately they must be faced. Even Bill Gates is finally seeing that, in a quite extraordinary pivot, as reported in the WSJ. Read here.

Better late than never, Billy.

Oil was, is, and always will be, unavoidably omnipresent in every facet of our lives and business, as Tommy Norris explains well.

(Fact check: some dispute that wind farms never recover their carbon footprint, but that shouldn’t weaken the thrust of his macro point, for anybody but the obtuse and the delusional.)

It’s alternative energy, not clean energy. There is nothing clean about it.

Oil finances sport.

Oil is the direct source of funds for the current biggest investor in our industry.

So anyone who really wants to analyse sport should know how all these dominos are lined up, and where they will fall. Understand petroleum and the petrodollar really well, to give yourself any decent chance of making the right decisions. Before the domino hits you.

Recognise fully the role of modern Saudi Arabia, and the importance of the oil price trend to your own career and personal livelihood. (e.g. if your world currently revolves around the continued success and investment in mega-projects like Neom, work out some contingencies perhaps?)

This is today’s Sunday Column.

Walls of money that distort.

Context is the key to everything. Also here.

Every competent finance operator of my generation bases what assets are worth around honest analyses of real profits (free cash generated), and the solidity of balance sheets. Modelling for us was about discounted cash flows (DCFs) and multiples of genuine earnings. Solvency risk got covered by things like the interest coverage ratio. Old school. Nothing fancy.

In this new millennium, however, all that has been overtaken by a very different set of rules. The dynamics of supply and demand, and the liquidity of capital.

For a good while now, valuations of absolutely everything have been dictated much more by overwhelming flows of money and artificially low interest rates than by any classic fundamental metrics. If there are significantly increasing amounts of capital flowing into an asset class, creating demand and momentum, with a relatively fixed supply, valuations are going to go up, regardless of “fundamentals”.

This has absolutely been the main macro axiom of the last 30 years, but its profound truth hasn’t been really noticed. Certainly not fully understood. Even knowingly “gamed” by the ruthless players in the darkest corners of Big Finance.

We are all now playing a very different game.

The modern cycle no longer runs on growth, but on liquidity.

Remi Tetot, from The Mad King newsletter, November 2025

Forever blowing bubbles.

The Hammers ain’t got anything on central bankers.

Since the dotcom bust at the turn of the millennium, our governments have created amounts of money out of thin air that are scarcely conceivable.

And that was 18 months ago. Some of the top thinkers in macro finance now put the liquidity injection in this millennium at $100 trillion!

The truth, since 2000, is that at the first sign economies were weakening, our leaders turned on the counterfeiting presses, pumping liquidity, to avoid any semblance of the normal business cycle. The internet bust in 2000/01, the Great Financial Crisis of 2008, Draghi‘s “whatever it takes”, COVID. Anything, basically.

Very simply, all government economic policy is now principally geared to propping up asset valuations. Not by using savings or reserves, but with freshly printed money created with the click of a mouse at central banks. They call it impressive names like “Quantitative Easing”.

It’s not impressive. They are merely debasing the currency and hoping no one will notice. One hesitates to nominate the Weimar Republic, but history has been here before. Even the Romans reduced the amount of actual silver in their coins for the same reasons. Debasement of the currency.

The Everything Bubble.

This Niagara of new printed money has had to be invested somewhere, and it has created what is known by some as “The Everything Bubble”. The name for the fact that every asset in the world, from housing, to classic cars, sports assets, Palantir, Nvidia, Picassos, is arguably now priced way too high.

For example, there is not a serious corporate finance expert who thinks a mature company like Apple, losing its innovation and design mojo, not really growing, should be valued at over 35 times earnings. For guys like me, that’s as bad a sin as cappuccino after supper, or a striped tie on a striped shirt. Heresy.

And yet, it couldn’t be any other way. If you create so much new “demand” with fresh paper capital, with liquidity, it’s inevitable that valuations get stretched. Simple arithmetic, and basic supply and demand.

No one wants to admit any of this, least of all central bankers and politicians, but the signs are all there in plain sight, and have been since 2008. The Great Financial Crisis wasn’t solved: a can was merely kicked way, way down the road. To where we are today, in a completely new paradigm for the capital markets.

So what about tomorrow? How do serious operators and investors (in sport) position themselves for what’s coming?

Reading signals.

In this new macro-finance world, no longer working on fundamentals, the secret of being successful is now based on one thing only. Reading the right signals and predicting whether these immense flows of money will continue to increase or, God forbid, even reverse.

For the last 25 years, everybody in finance got the same memo. The same clear signal:

“Don’t fight the Fed. They have your back. Relax.”

The idea that you could manage your capital, take on excessive risk, lever-up with debt, knowing that the Federal Reserve of America wouldn’t let valuations drop.

“They’ll use the Fed put, so buy the dip.”

And we have. Or, more correctly, the algorithm has.

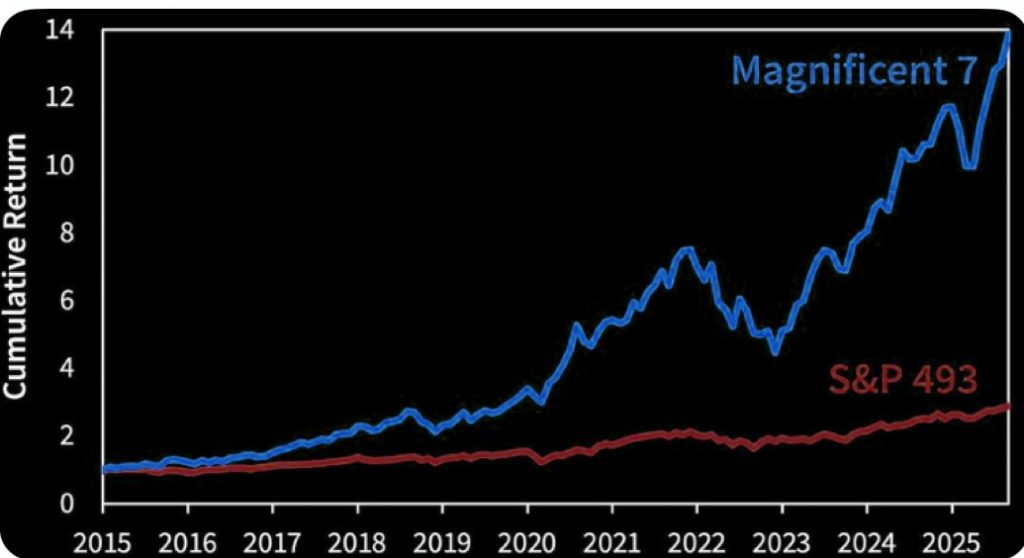

Half of the world’s institutional capital is now invested in passive index funds run on “rebalancing” autopilot. Think about that. Trillions of capital being moved around without a human in sight, which has all totally polarised markets to be dependent on very few big companies. Markets should be wide in depth, not narrow like the Magnificent 7. Getting worse every day.

So a great investor these days is in reality playing a game of chess against the computer, trying to work out what Skynet is going to do in the next 5 moves, to recalibrate the index. And on what AI inputs?

(Let’s park AI for a brief moment.)

Ultimately, like this, we need to accept that some lines of code may one day decide that it’s time to change the flows of money into our industry. And we will need some kind of radar to get ahead of all that.

The Albachiara Radar.

Every serious macro investor has their own signposts. The charts they watch, the notifications they set up, the alerts to which they always react. Their stop-losses.

These are ours, the Albachiara Radar:

*

The interest yield being demanded to hold the debt of countries and companies.

The higher it goes, the more one should be very, very scared.

A favourite chapter in Sport’s Perfect Storm is the story of bond vigilantes and Liz Truss, and how the yield on the debt of Big Media companies was telling us what was going to happen, which then played out. Indeed, there are some elite market operators who do nothing else but look at yield charts, especially if the yield on American government debt of 10 years duration is approaching 5%. The best experts know that yield now really needs to be in a very narrow range of 3-4%. Another Goldilocks axiom.

One can easily see from the graph how the reducing cost of capital trend, from the high of 15% in the mid-80s, to basically zero, changed abruptly 3 years ago. A 35-year bull market in cheap cost of capital started turning, and this has utterly fucked-up altered the worlds of private equity, venture capital, and corporate finance in general. They haven’t yet admitted that to us, as they don’t have to mark-to-market, and of course, mum’s the word. The losses are all in their continuation funds. Private equity and debt, known to many as the shadow banking system, are singing a very ominous song these days. Caveat emptor.

**

The price of gold.

This is a contrarian siren signal on the health and trust of our whole economic system. Gold is the ultimate “hedge” against everything going to shit south. If the price/cost of that hedge is increasing, as it is, this is the market telling you that the ice is getting very, very thin. Look how gold has nearly quadrupled in the 8 years of the AYNE podcast.

And they called us “doom pornsters”! Forgive them, Father, for they know not what they do.

And they called us “doom pornsters”! Forgive them, Father, for they know not what they do.

***

The price of oil.

This is Tommy Norris’s financial and geopolitical bellwether of absolutely everything. Since 1971, for over 50 years, the politics of oil have utterly dictated our entire world. Wars are fought over it. People are assassinated for it.

The movie Syriana earned George Clooney an Oscar and is as honest as it gets about what is done in the name of the control of oil, and its price. Syriana isn’t a film; it’s a documentary.

In short, the US‘s 10-year yield getting near 5% spooks everyone, and gold trebling in 4 years is a clear sign of increasing lack of trust in our financial infrastructure. But most great analysts especially take notice when the black stuff out of the ground moves too far away from Goldilocks. From $80.

That really freaks people out, because they know there will be serious economic and geopolitical consequences either way. Especially in times of conflict with major oil producers like Iran and Russia.

Oil always dictates what happens next.

Especially in what the Kingdom will do.

Saudi Arabia needs oil prices at $80+ a barrel to finance everything it wants to achieve as a country.

Its whole Saudi Vision 2030 geopolitical strategy, and its investments in sport. Read here:

Oil is at $60, so it should now be apparent what today’s Sunday Column is really all about.

Not often, but increasingly so, you overhear conversations in our industry suggesting that the Saudis just don’t have the money. And sport is going to suffer.

Is the petrodollar “bid” for sport drying up?

Do our Middle Eastern friends still have the wedge? And if they do, what changes in strategy will they be obliged to adopt?

This is an utterly existential analysis for the industry and the asset class of sport, with worthy op-eds everywhere, especially after the Davos in the Desert (FII) conference.

Isn’t it interesting how fast things can evolve?

Nearly three years ago, when the only word used around Saudi and this industry was “sportswashing”, a similarly themed Sunday Column set out the Albachiara view of where all this was going. And why Saudi was a net positive.

Since then, we have seen the rise of LIV, the SPL football league, DAZN, Newcastle United, the ATP, the PTO, myriad indirect investments via sponsorship, and sports funds where Saudi is an LP investor. It has all played out fully, perhaps even more so in gaming and e-sports. The announcement of the EA Sports deal is simply era-defining, reported well here….

So let’s be clear, Saudi is going nowhere.

Oil may be twenty bucks short of where it needs to be, but this country is utterly committed to being a major player in sport, media and entertainment, and already has influence and capital deployed everywhere. Sport is the catalyst for their social change, health and well-being, in a country with a very young population. Ignore the people who so badly want the inverse to be true, because they’ve never ever liked Saudi Arabia, and much prefer the London-centricity of sport on this side of the Atlantic.

The EA deal is especially telling. A co-investor with PIF is Silverlake, the personal funding partner of Ari Emanuel’s whole sport and IP play, and behind all the Prestige dictating the rise of Paramount. The gang has been rounded up.

→ The really useful task today, with oil at $60, is understanding how the Kingdom now shifts its priorities and timeframes. How it ADAPTS!

Rebudgeting around tighter money.

Saudi Vision 30 isn’t going to change, it just may now need to be rebranded as Saudi Vision 50! There is no option with oil at $60.

And as any good accountant knows, when belts are getting tightened, you look at materiality. You focus on those savings that really move the needle, and don’t sweat too much on the line-items that won’t, even if you cut them 40%.

The Realpolitik of the CFO that Jim Ratcliffe perhaps hasn’t understood at United. (Dinner Ladies Jim? Really?)

So the Saudi leadership will look at materiality and hit the mega-projects first:

*

The absurd budget overruns in Neom, Quiddiya, and others need to stop. And they will.

Their timeframe will now be extended, and there will be a new maniacal focus on efficiency, as the waste has been eye-watering. This is by far the top priority.

**

The Kingdom will then make a stronger push to ensure tighter collaboration and the removal of internal silos.

The Ministry of Sport, PIF, SURJ, Aramco, (royal) family offices and the General Entertainment Authority will all be told to join up their thinking. With alacrity. This always happens when any project goes from the marketing set-up phase to operational and commercial maturity. Structures and processes get tightened, heads get knocked together.

***

New investments in sports IP may be less frenetic, with likely emphasis on a consolidation period of “making what we already have work”.

In that thinking, domestic-focused participation sports like the SPL will likely get more of a priority than global projects like LIV. But any cuts here will be at the margins, as the amounts involved are chump-change compared to the mega-projects. I really wouldn’t worry so much about Saudi pulling back from sport IP.

****

But sports and sportech, looking for capital from the Kingdom, now better bring their A-game to their pitch.

Money is tighter, and investment evaluation will be sharper. It’s a higher bar. Direct personal involvement in the SURJ investment into the PTO showed me that Saudi isn’t casually throwing money around. That was a keenly negotiated deal with deep discussions into operational value-adds. As it should be. If you want Saudi investment, be a top pro and you’ll have a good chance.

*****

AI?

Ah yes…

Chasing the AI dream.

The Kingdom is now making serious investments into AI and its infrastructure. Read here:

At first glance, this seems obvious. AI will absolutely change everything in our economies and lives. No doubt. But is it a smart investment? Could this instead be another endless drain of resources? Something as potentially harmful as over-investment in the mega-projects?

A good friend will always risk explaining harsh realities and warning about possible errors. Offering up one of those unpopular, unpalatable minority reports. Here is a free one from Albachiara.

Bide your time with AI!!!

For the brightest analysts, with the best signals, one of the most concerning developments in the global economy is the very clear and obvious “over-build” in AI capex, that risks to never ever generate a financial return. Many of the world’s biggest companies, the core of the Magnificent 7, (Amazon, Meta, Alphabet, Microsoft), now realising exactly this, are themselves entering a more sensible “consolidation” phase in this bubble. Cutbacks and layoffs are everywhere after trillions spent in total.

AI as a thematic asset class now represents c50% of the S&P 500. That is again insanely narrow polarisation, and in some places, this scepticism is now being well articulated.

For Saudi Arabia, or anyone, there is potentially a better play around investment in AI, learning from what happened 25 years ago around fibre optics investments driven by the birth of the internet.

Wait till the bubble bursts and pick up the infrastructure assets that have been built (by others) for cents on the dollar.

Those Landman windfarms.

The AI risk for investors doesn’t even stop at “over-capacity”.

There is now serious academic research that points to the horrendous carbon footprint and water-usage around data-centres, rarely mentioned by the market cheerleaders. Luckily credible people like MIT do:

The energy resources required to power this artificial-intelligence revolution are staggering, and the world’s biggest tech companies have made it a top priority to harness ever more of that energy, aiming to reshape our energy grids in the process.

One is reminded of those Texas windfarms and Tommy Norris’s monologue.

The fact is that any economy or business on the planet lives or dies on its access to cheap energy. It’s really that simple. The rest is noise. Ask Germany and its carmakers about that now.

AI is going to be no different.

To protect your business and career, always watch the oil markets, the price of a barrel, and the currency in which it trades.

“Drill baby, drill.”

To order the Limited Edition of Roger Mitchell’s book “Sport’s Perfect Storm“, click here and fill the form.

Listen to our “Are you not entertained?” management podcast here.

To find out what we do in change management, have a look here.

For our C-suite management services, read here.

Here you can know more about our content development work.

Discover our Corporate Learning service here.

Get to know more our “Sport Summit Como” yearly sports management event here.

If you want to read our own story, go here.